The point of the situation

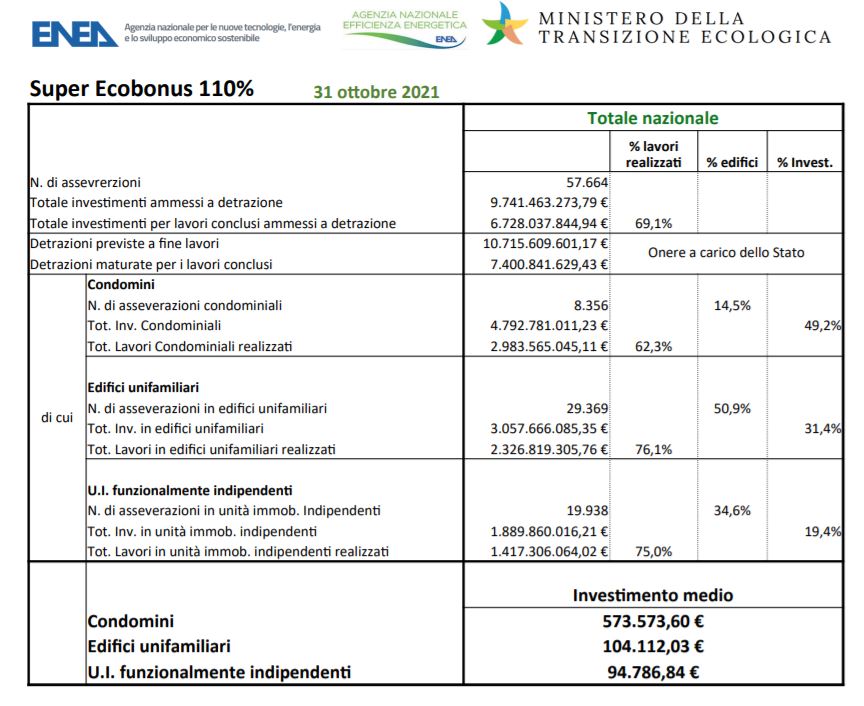

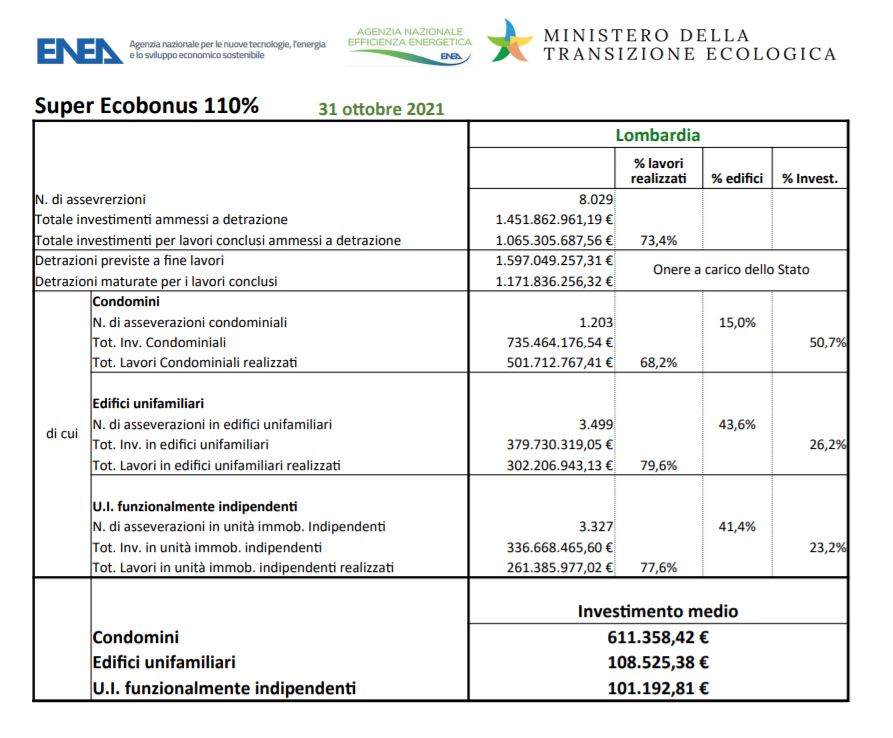

As of 31/10/2021 the figures for 110% speak of approximately 10.7 billion euros (about 2.5 billion more) as deductions provided at the end of the works (ft ENEA), 57,664 construction sites (number of asseverations) have been started one year after the start of the superbonus on 110% . Lombardy, with 1.4 billion in investments eligible for deductions and over a billion for work carried out, for a total of 8,029 asseverations, outstripped all other regions.

The numbers continue to grow, but the focus of media attention is on the parliamentary debate that will lead to the definition of the 2022 Budget Law.

There are many questions, but what interests us today is the extension and revision of the 110% superbonus and the attempt to find an agreement between the alternative options to the tax deduction.

The alternative options have in fact opened up the work to all parties, even those without major spending power.

Under Article 121 of the Relaunch Decree, beneficiaries may opt for:

These two options, according to the same Decree, are valid for the other tax bonuses.

The problem arises when some bonuses (ordinary ecobonus and sismabonus) already provide, as in fact they do, alternative options where the beneficiary of the deduction can only opt for a discount on the invoice from the supplier who carried out the work. The latter may either offset the tax credit (in five equal annual instalments) or transfer his tax credit to his suppliers of goods and services (the latter will then not have the option but may only offset it). The picture is very different from what would be envisaged by the options provided by Article 121 of the Decree.

Remaining on the alternative options, the draft Budget Law provides for an extension to 2025 limited to superbonus interventions. While for all other tax bonuses, the alternative options, as provided for in Article 121, will end on 31 December 2021.